bitcoin has no detectable cycles in daily data

a frequency analysis

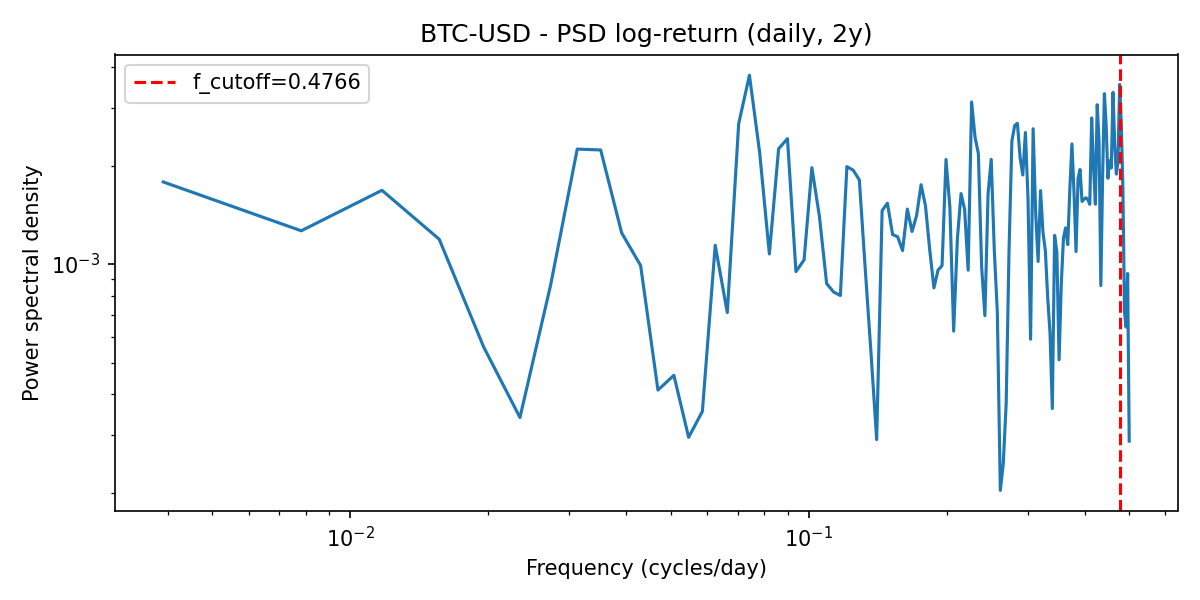

I ran a spectral analysis of Bitcoin using two years of daily log-return data. The goal was to identify whether the BTC/USD market exhibits any periodic structure: recurring rhythms, dominant cycles, or predictable frequency bands at the daily resolution.

the frequency-domain result

The global power spectral density (PSD) shows that 95% of the signal’s total energy resides below:

This corresponds to oscillations with periods longer than roughly:

In other words:

Bitcoin’s daily movements are almost entirely driven by slow, multi-day dynamics.

There is no meaningful high-frequency structure in daily data.

implication for sampling rates

Using the cutoff frequency, the Nyquist criterion gives an optimal sampling interval of:

Which leads to a practical conclusion:

Daily sampling (1 point every 24 hours) captures almost all meaningful structure contained in daily log-returns.

Finer sampling does not reveal additional “signal” at this scale; it only increases noise relative to trend.

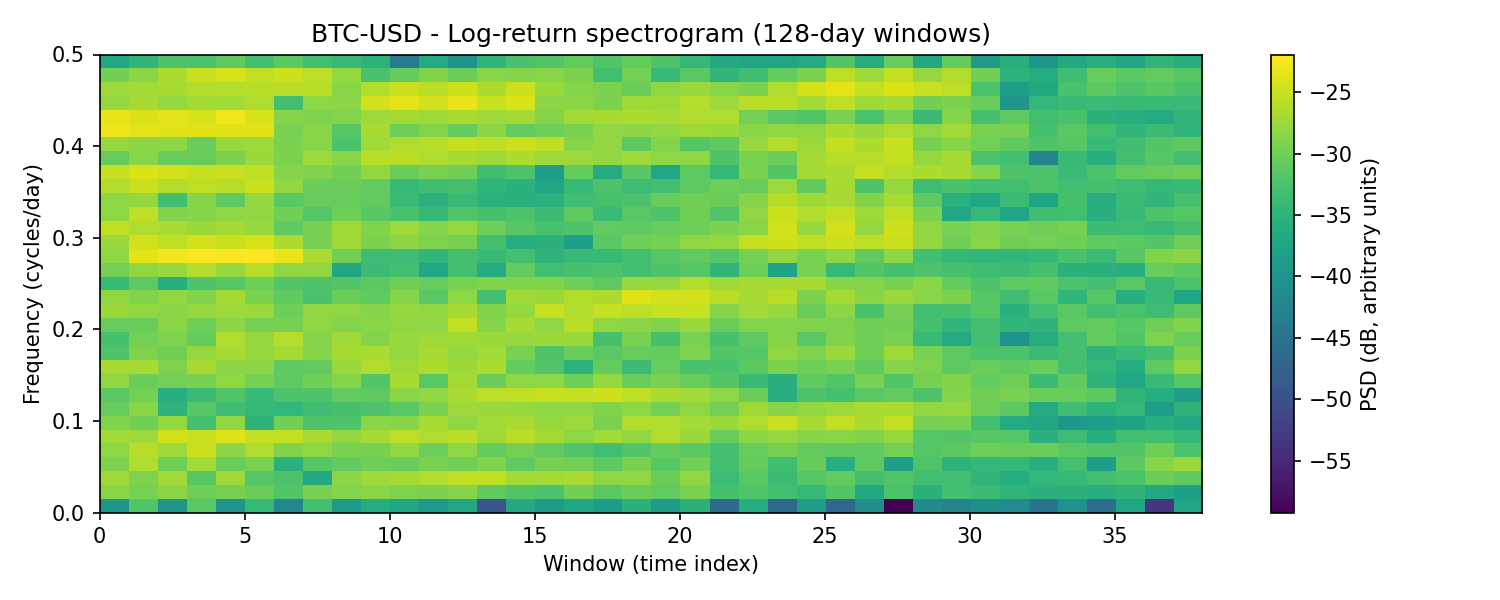

what the spectrogram shows

Using sliding windows of 128 days, the spectrogram displays how spectral power evolves over time.

The key observation:

There are no stable spectral bands.

No persistent cycles.

No consistent periodic structure.

Instead, the heat map shows diffuse, shifting power which is typical of a stochastic process with volatility regimes, rather than a cyclical one. The “structure” in Bitcoin’s daily behavior comes from changes in volatility and trend, not from oscillatory components.

why this matters

Many trading narratives implicitly assume cycles:

“monthly rhythm”

“weekly tendency”

“3-day rotation”

“cross-market heartbeat”

But frequency analysis cuts through intuition and directly inspects the structure of the data.

The conclusion here is unambiguous:

At daily resolution, Bitcoin behaves as a non-periodic, noise-dominated process with slow volatility regimes.

what we cannot see with daily data

Daily sampling inherently limits the observable frequency band to:

Meaning:

anything faster than one cycle per day

any intraday periodicity

microstructure oscillations

liquidity cycles

exchange-specific flows

are all aliased and therefore invisible.

To explore whether Bitcoin exhibits meaningful intraday frequency structure, we need higher-granularity data. semn.ai aims to uncover this data in its vizualization terminal and provide an almost continuous sampling process.

final takeaway

The data shows:

no cycles at daily resolution,

no persistent frequencies,

no resonant behavior,

only slow regimes and noise.

Daily data is excellent for capturing long-term drift and volatility shifts, but useless for detecting cyclical behavior. For micro-structure and a hidden peek into real-time market moving forces I am building semn.ai, which uncovers the heartbeat of bitcoin, without candles and beyond noise.

Waitlist is open for a limited time and taking applications for early access.